What Is Liquidity Providing? Beginner's Guide to Earning Crypto Fees

Today, I'd like to talk about one of the most innovative concepts in crypto: liquidity providing. In my opinion, earning fees by providing liquidity is one of the biggest breakthroughs in DeFi.

Before we dive into this issue, I wanted to share something new I’ve been working on—Indexy. A new app designed to make tracking, investing, and learning about crypto markets easier and more effective.

Right now, keeping up with crypto feels outdated. With new sectors constantly emerging across different blockchains, tracking one coin at a time just doesn’t cut it anymore. We need better tools to follow trends, reduce risks, and get a clearer picture of the market.

Try out the Beta 👉 Indexy.xyz

Let's dive into one of the most innovative concepts in crypto: liquidity providing. In my opinion, earning fees by providing liquidity is one of the biggest breakthroughs in decentralized finance (DeFi). However, there's a catch: the barriers to entry are extremely high. The mechanics are complex, you need significant capital to be effective, it's easy to lose money if you're not careful, and the metrics shown by many protocols can be confusing.

In this article, I'll cover the basics of liquidity providing, compare DeFi to traditional finance (TradFi), and explain how one of the most popular DeFi protocols—Uniswap—works. This won't be a highly technical guide but rather an easy-to-understand intro, so you can decide if liquidity providing is worth your time and money.

Liquidity in Traditional Finance

Before diving into crypto, let’s quickly cover liquidity in traditional finance.

ATMs

Think about getting cash from an ATM. ATMs were first introduced in the late 1960s but really gained mainstream traction in the mid-1980s alongside debit and credit cards, making accessing your money easier. While digital banking took off, banks initially rewarded customers with solid returns for keeping money in savings accounts. But over time, things changed dramatically. Fees increased, banks imposed withdrawal limits, and interest rates dropped significantly. Nowadays, earning even 3% to 4% annually feels like a win, especially considering inflation. Essentially, your money loses value sitting in the bank.

Yet, ATMs remain useful. Banks maintain vast networks to ensure easy cash access, even though ATMs have drawbacks like security risks (ever had your card cloned?) and hefty fees.

Exchange Houses

Another traditional example is currency exchanges. When traveling or holding different currencies, someone profits by charging a spread between buy and sell rates. This mechanism, while simple, depends on centralized entities like banks or exchange houses.

Decentralizing Liquidity

In crypto, we want similar services but without centralized control. Decentralization means no banks or single companies oversee the process. Instead, liquidity pools step in.

But who ensures liquidity is always available so that protocols, apps, and users can smoothly swap currencies? The answer: anyone can. Unlike traditional finance, where banks and centralized entities provide liquidity, crypto allows anyone—individuals or institutions—to provide liquidity and earn fees in return. That’s right; by depositing your assets into a liquidity pool, you help maintain the decentralized financial ecosystem and receive fees for your service. Pretty neat, right?

I find this idea fascinating because it democratizes financial services. However, there's a catch—it's not as simple as it sounds. Creating a decentralized system that functions smoothly, without any central authority stepping in to correct errors or manage issues, requires complex dynamics. These decentralized protocols rely on automated mechanisms like smart contracts, which must account for various scenarios and market conditions. While significant progress has been made, challenges remain.

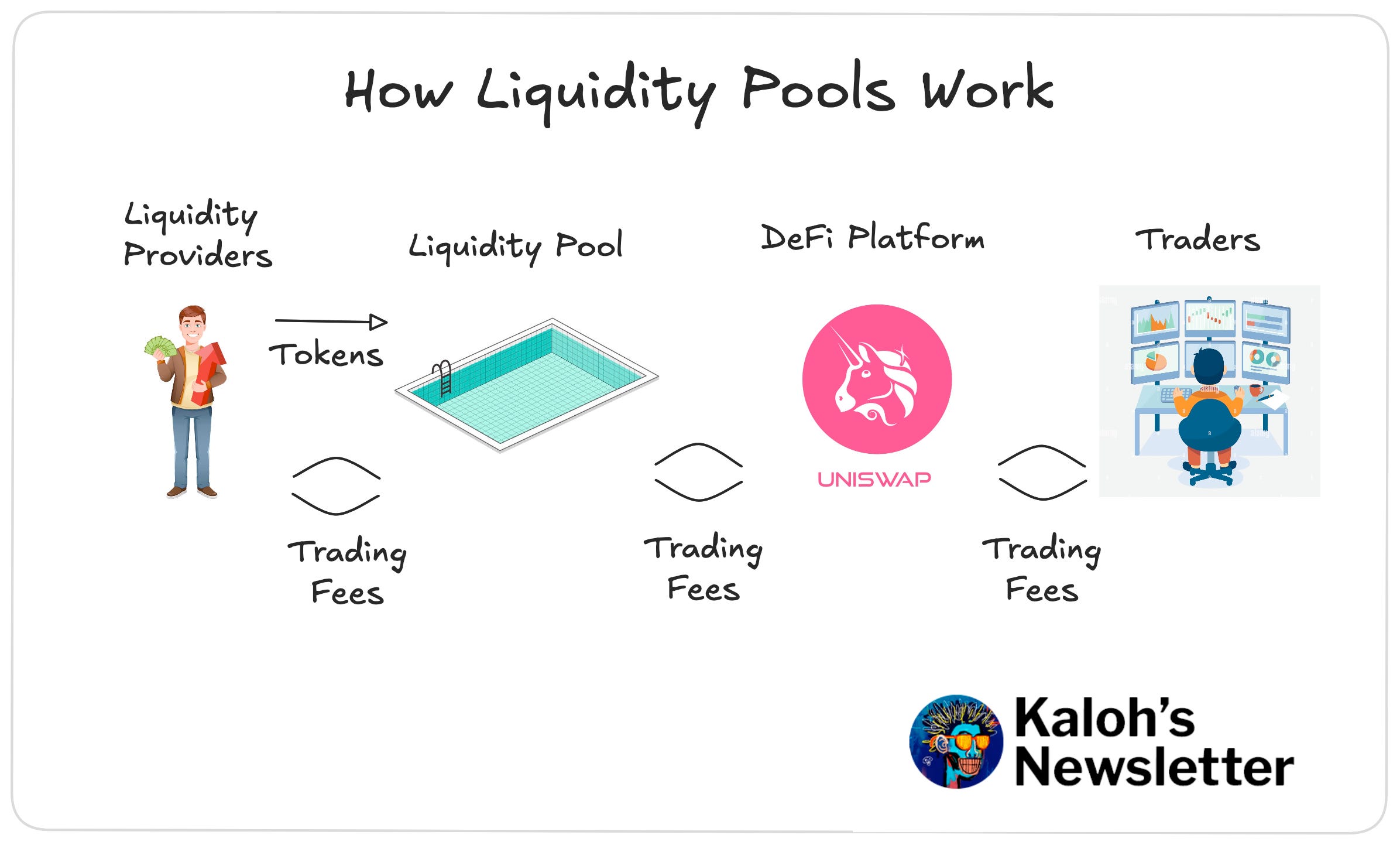

How Does Uniswap Work?

One of the earliest and most successful innovators in this space is Uniswap. Uniswap is a decentralized protocol that revolutionized asset swapping by introducing the concept of liquidity pools and liquidity providing. Instead of relying on centralized exchanges or intermediaries, Uniswap lets users trade directly through liquidity pools managed by smart contracts. So, how exactly does this work?

A liquidity pool holds two assets—let’s say ETH and USDC. When you exchange ETH for USDC, you interact with this pool. The price depends on the available liquidity, set by the market. Providers add liquidity (ETH and USDC) to these pools, enabling trades to happen instantly at market rates. Every time a trade occurs, a small fee is charged, and liquidity providers earn a share of these fees proportional to the liquidity they provide.

Example: If you want to swap ETH for USDC, you submit ETH and receive USDC at the current market rate. Behind the scenes, your ETH goes into the pool, and USDC comes out. A small fee is collected during this exchange. That fee funds the protocol and rewards liquidity providers for contributing their assets.

Why is Liquidity Providing Exciting?

It’s fully decentralized. The system operates without central authority, automatically balancing asset prices and rewarding those who provide liquidity. It’s revolutionary—but not without risks.

The main questions you should ask are:

Is it profitable?

What risks are involved?

I've experimented with liquidity providing over the past two years, becoming more serious about it recently. In upcoming articles, I'll try to answer this questions and provide a couple of strategies tailored to different risk appetites.

Until next time,

- Kaloh